If you are researching pet insurance in Singapore, one of the names you will probably come across is MSIG PawEasy. This MSIG pet insurance review is based on my personal experience covering three things that matter most to pet owners: claims, renewal communication, and non-renewal.

On paper, MSIG presents PawEasy as an auto-renewable pet insurance plan and highlights features such as renewal benefits and no-claim discounts. But after going through a full policy cycle myself, I came away feeling that the bigger issue is not just what a policy covers today, but whether that coverage will actually continue when the policy year ends.

That matters even more in Singapore because there are not that many mainstream pet insurance options to begin with. Local comparison pages repeatedly feature a fairly small pool of insurers — MSIG, Liberty, Income, Etiqa, CIMB, and a few others depending on how the market is grouped — which means pet owners may have limited room to switch once claims history, waiting periods, and exclusions start to matter. For a broader look at available insurers, see our pet insurance Singapore comparison guide when i first researched about it.

Disclosure: This is a personal account based on my own experience as an MSIG PawEasy policyholder in Singapore. It is not affiliated with or endorsed by MSIG Insurance. Policy terms, renewal decisions, and claim outcomes can vary — always verify details directly with the insurer or your agent.

Quick Overview: MSIG PawEasy at a Glance

| Product | MSIG PawEasy — accident and illness cover for dogs and cats |

| Marketed as | Auto-renewable, with renewal benefits and no-claim discounts |

| This review covers | Claims experience, renewal communication, and non-renewal |

| Key takeaway | Valid claims were paid, but renewal continuity was not guaranteed in practice |

What This Review Covers

This post is not meant to tell every pet owner to avoid or choose MSIG. It is simply a personal account meant to help new pet owners think more carefully about one issue that is easy to overlook at the start: yearly renewal is never something you should casually assume, even when the product is described as auto-renewable.

That point matters because pet insurance has a high switching cost. Once a pet develops conditions, changing insurer can become much harder because new policies often come with waiting periods, exclusions, and fresh underwriting.

Why I Chose MSIG Pet Insurance

As a first-time pet owner, MSIG looked like a reasonable option. It is a known insurer, the product page appears straightforward, and the plan is publicly described as auto-renewable — which naturally gives the impression of continuity as long as premiums are paid.

That is also why the later experience felt so surprising. My expectation at the start was simple: if I submitted legitimate claims properly and kept the policy active, renewal would at least feel predictable.

Claims Experience

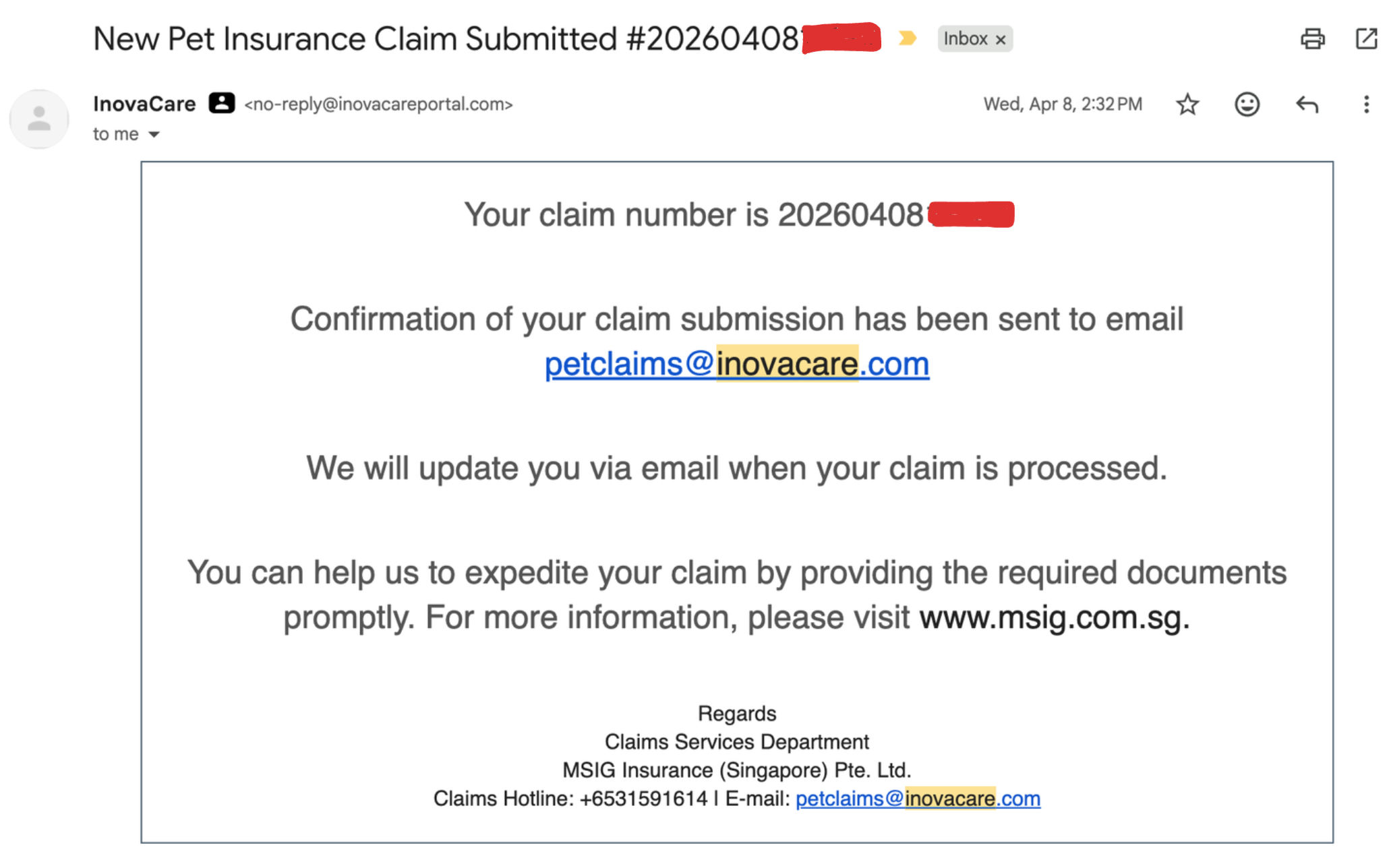

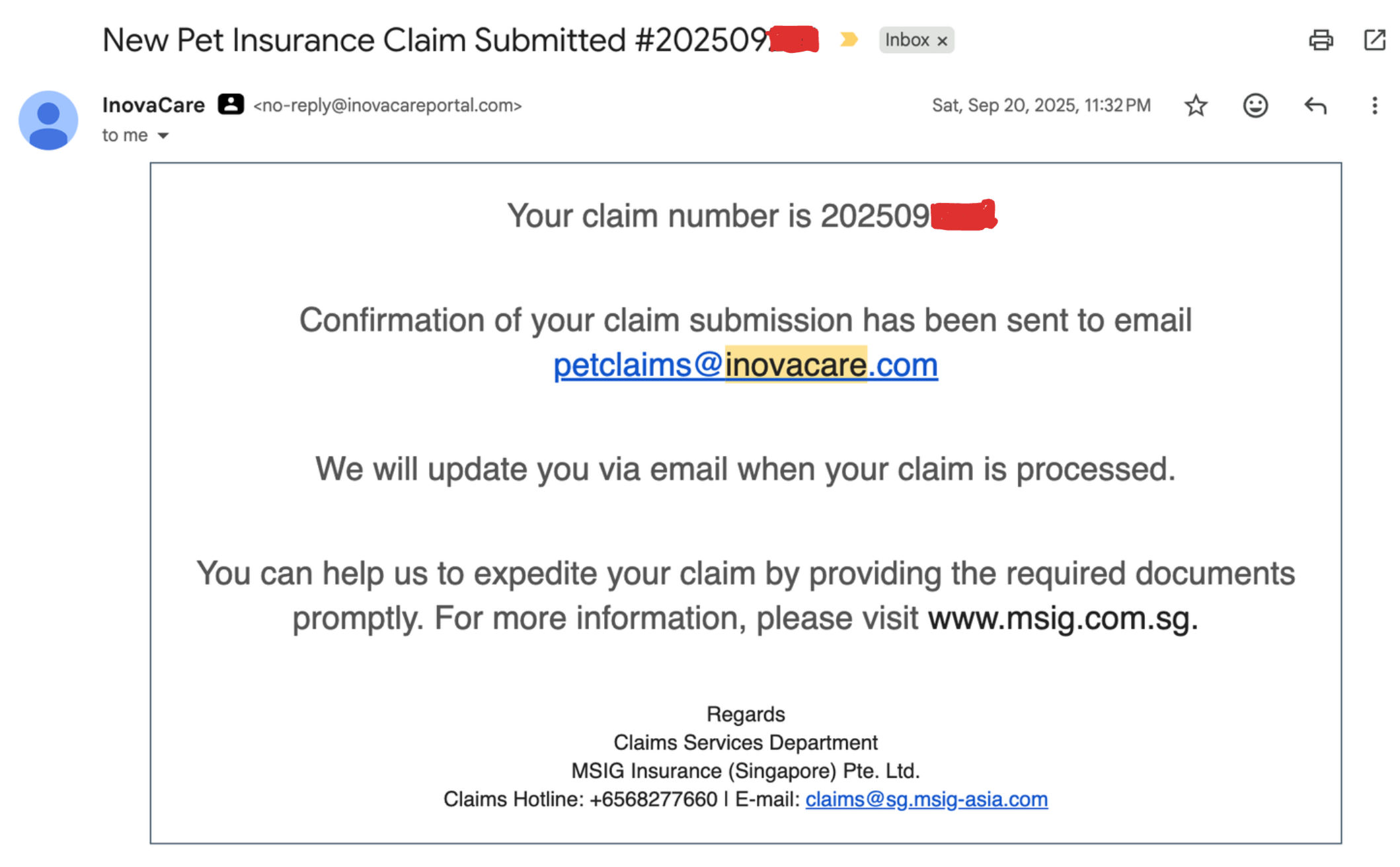

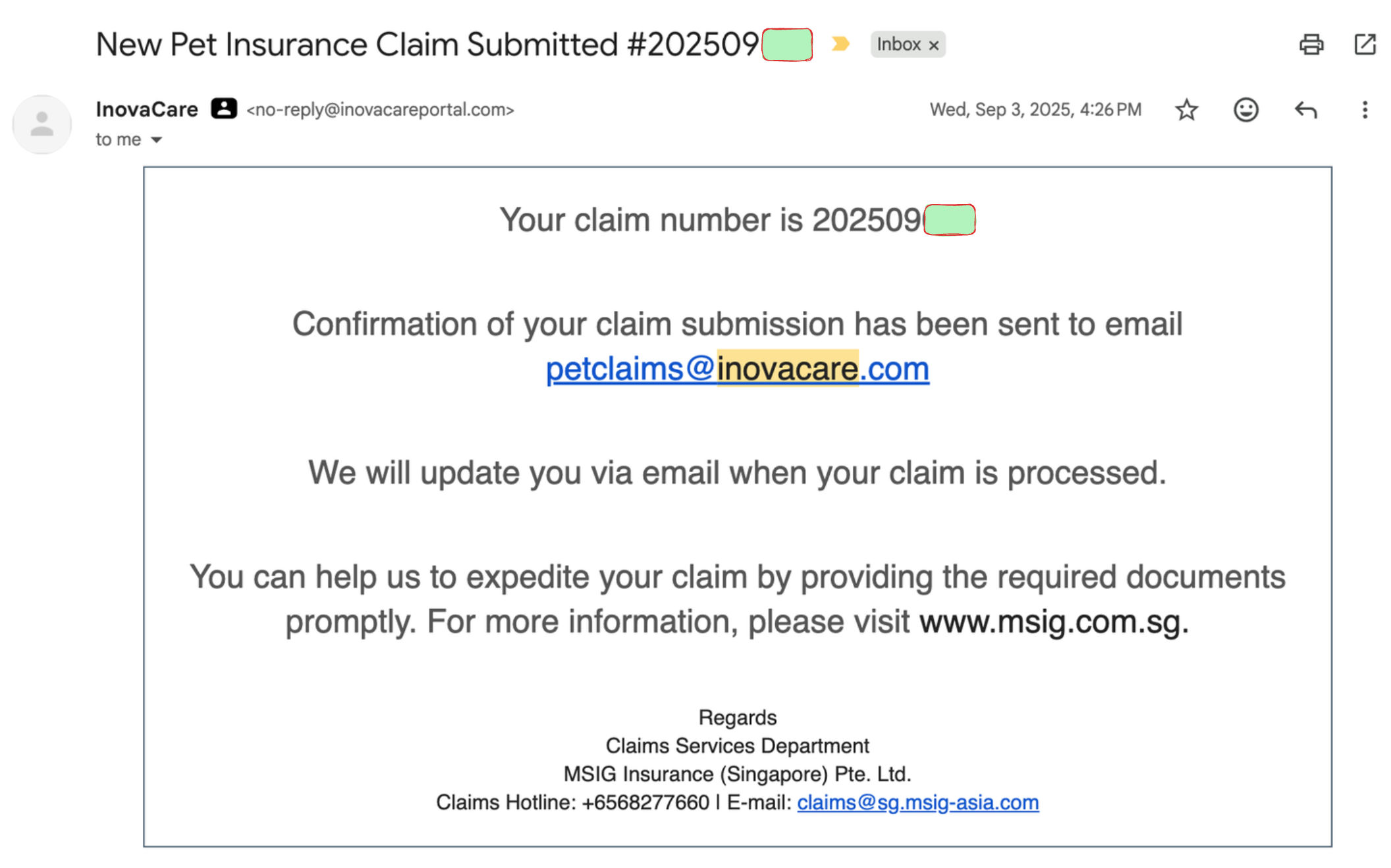

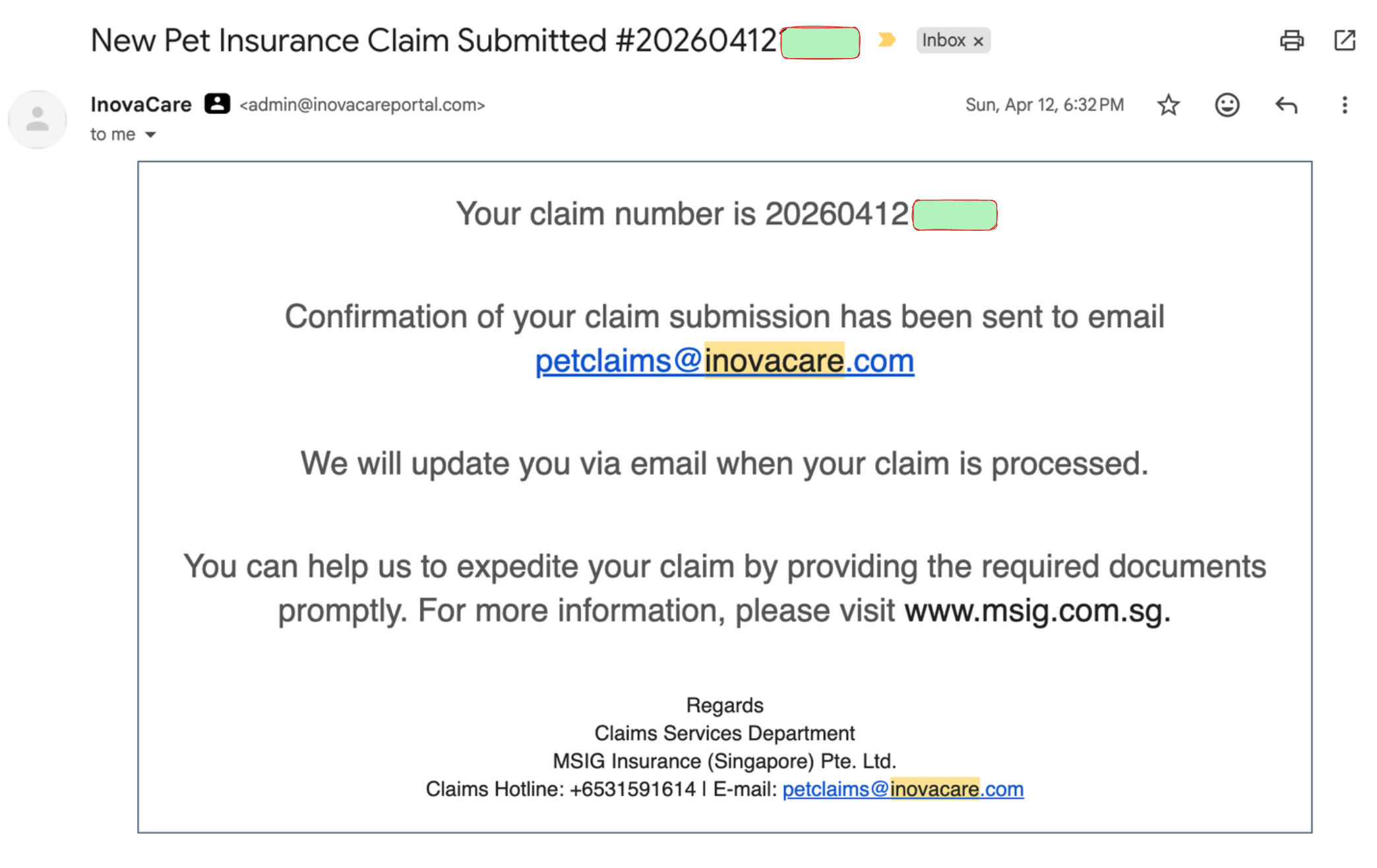

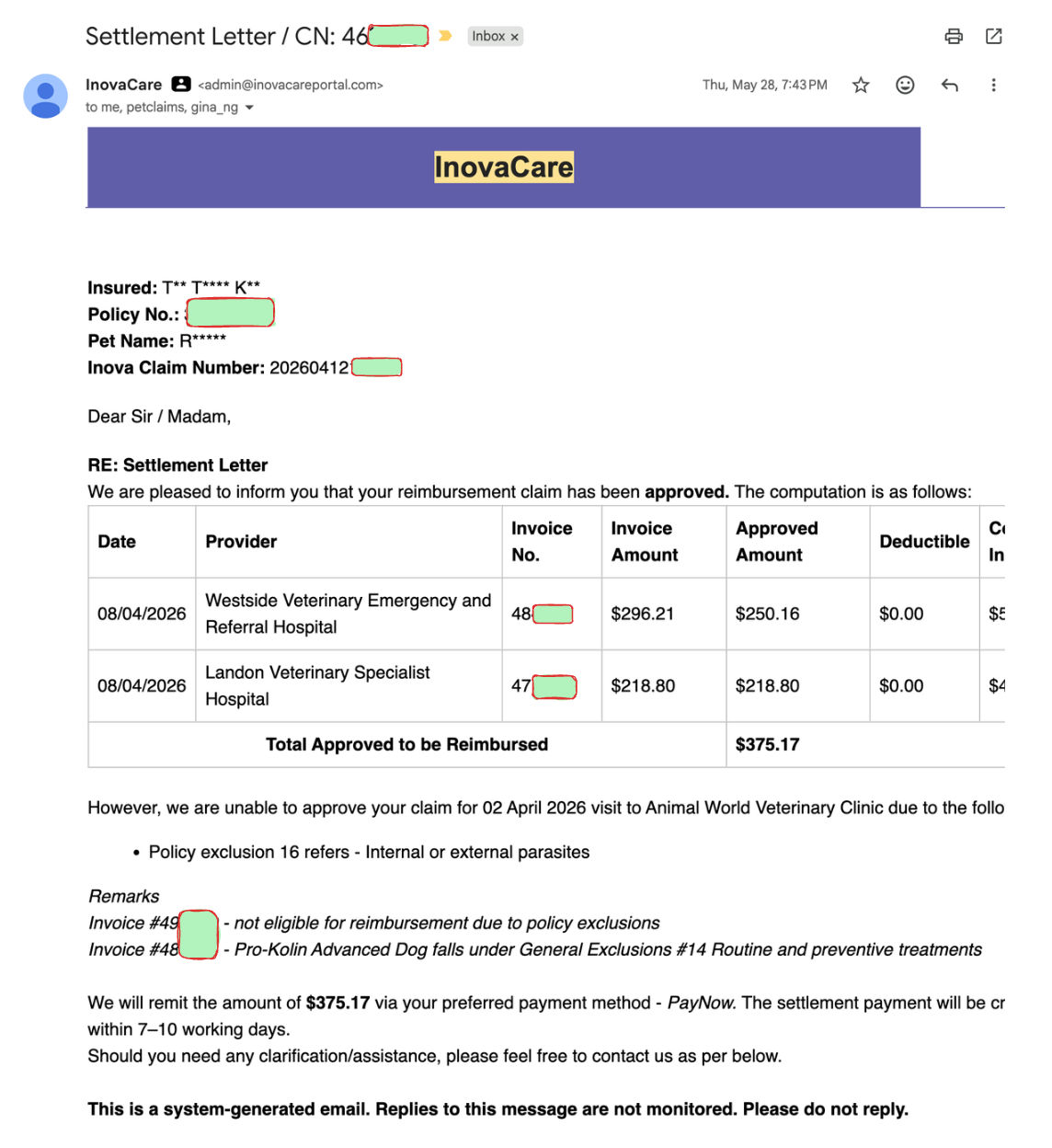

Over the course of one policy year, multiple claims were submitted. Out of those, 2 claims were approved and paid, and the submissions were supported with claim forms and vet receipts.

That distinction matters. The point here is not that every claim was approved, but that even with only 2 approved claims across one full year, the policy still ended up not being renewed based on what was later conveyed through my agent.

To keep this post transparent and evidence-based, I will be attaching screenshots showing:

- Number of claims submitted

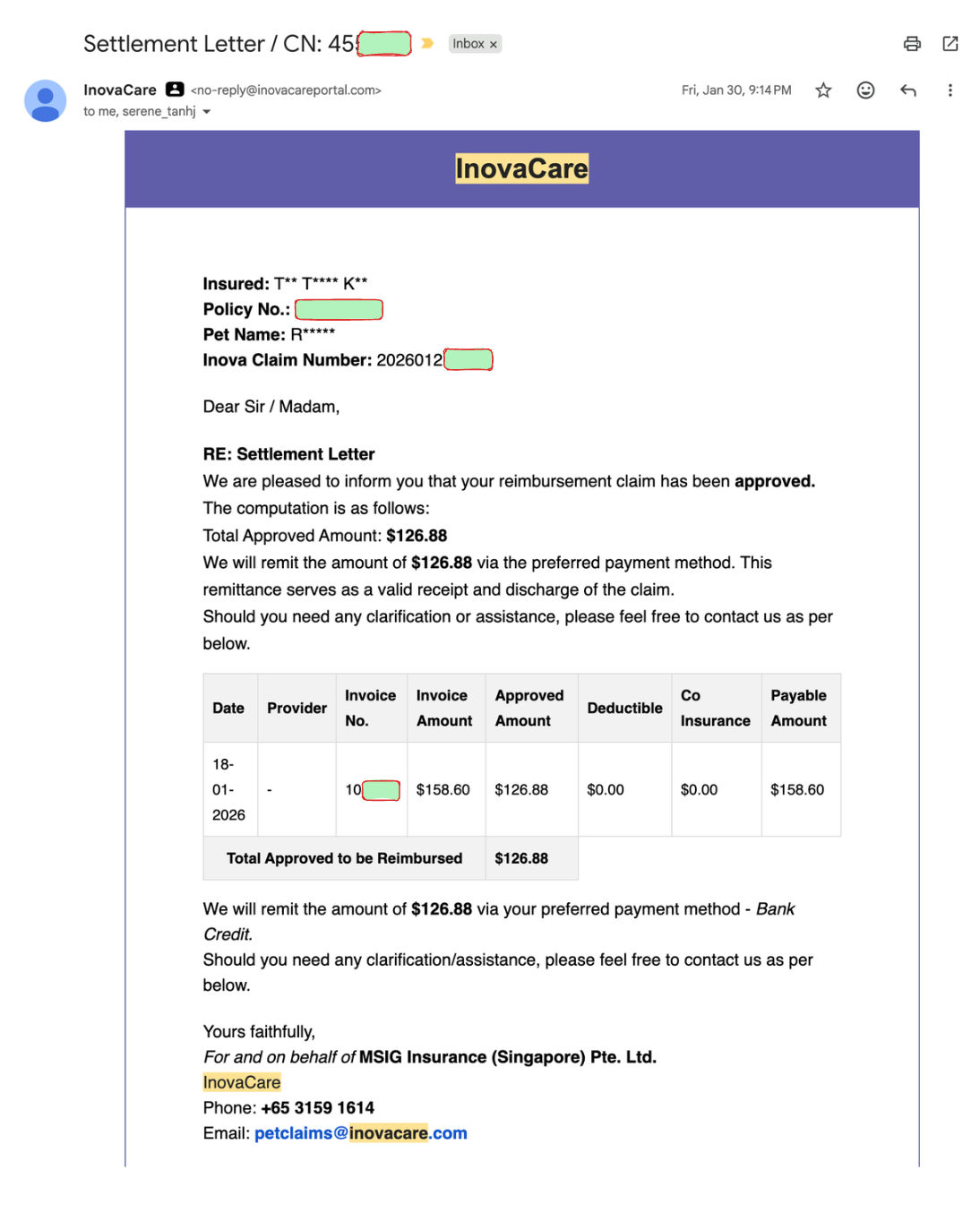

- The 2 claims that were approved

- Claim amounts reimbursed

- The renewal-related emails received

To be fair, MSIG did process and pay out valid claims. I do not think it would be accurate to say the insurer never paid, because that was not my experience.

The claims form are terrible to fill in. The form does not allow "#" in the field but didn't state that properly. I wasted a lot of time trying to fill in the form. I ended up building a Chrome Extension cause I want to make filling up form easy and seamless for future claims with the intent I will be using this insurer for years to come. Who knows what happen towards the end of the policy year.

If you are currently insured with MSIG and find the claim form tedious, we built a free MSIG Pet Insurance Claim Chrome Extension that auto-fills policy numbers, microchip details, and other mandatory fields — but that convenience does not change the broader renewal considerations discussed in this review.

Here are all the screenshots of the claims submission acknowledgements:

Here are the 2 claims that were approved and paid:

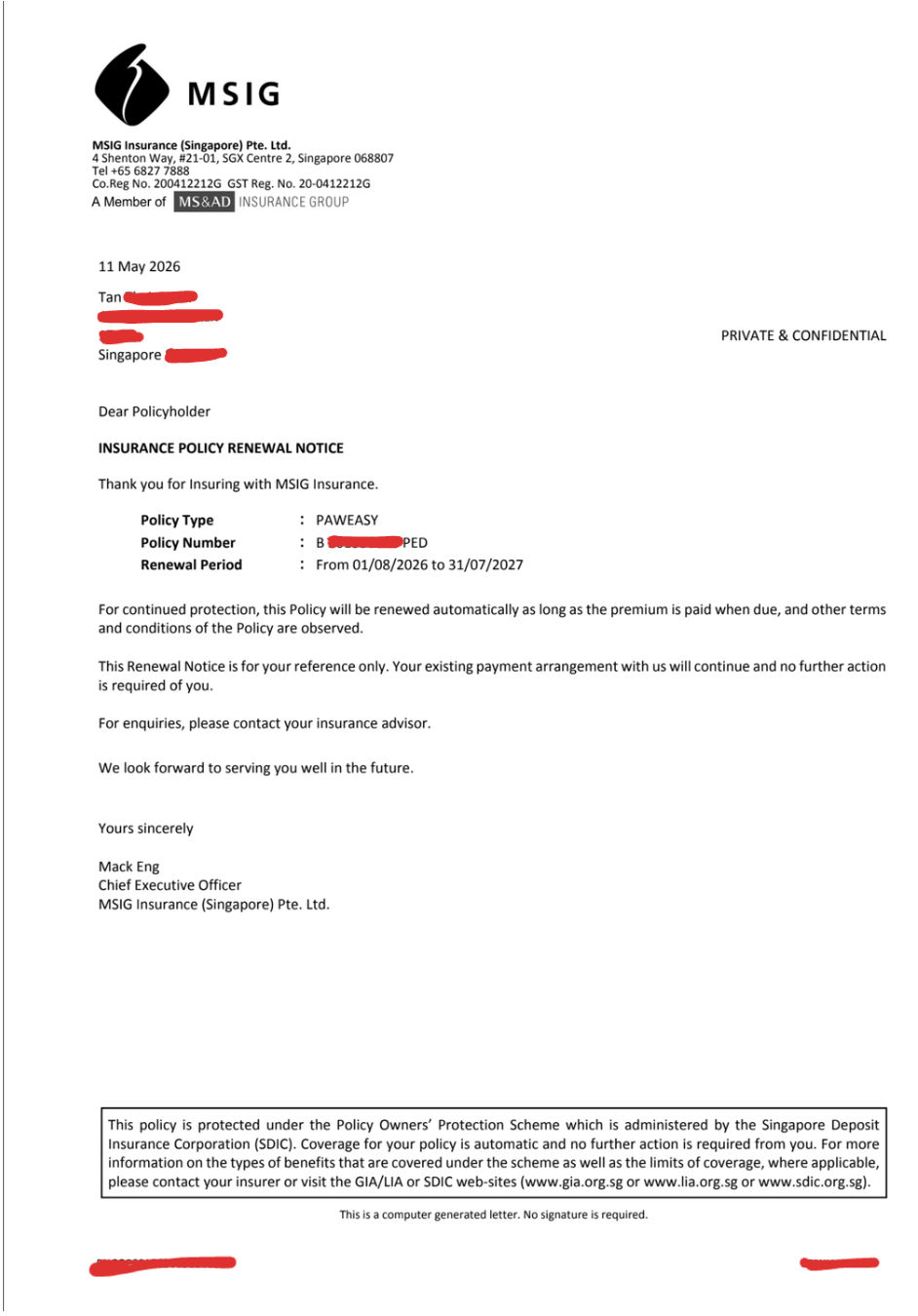

Here's the renewal notice I received on 11 May 2026:

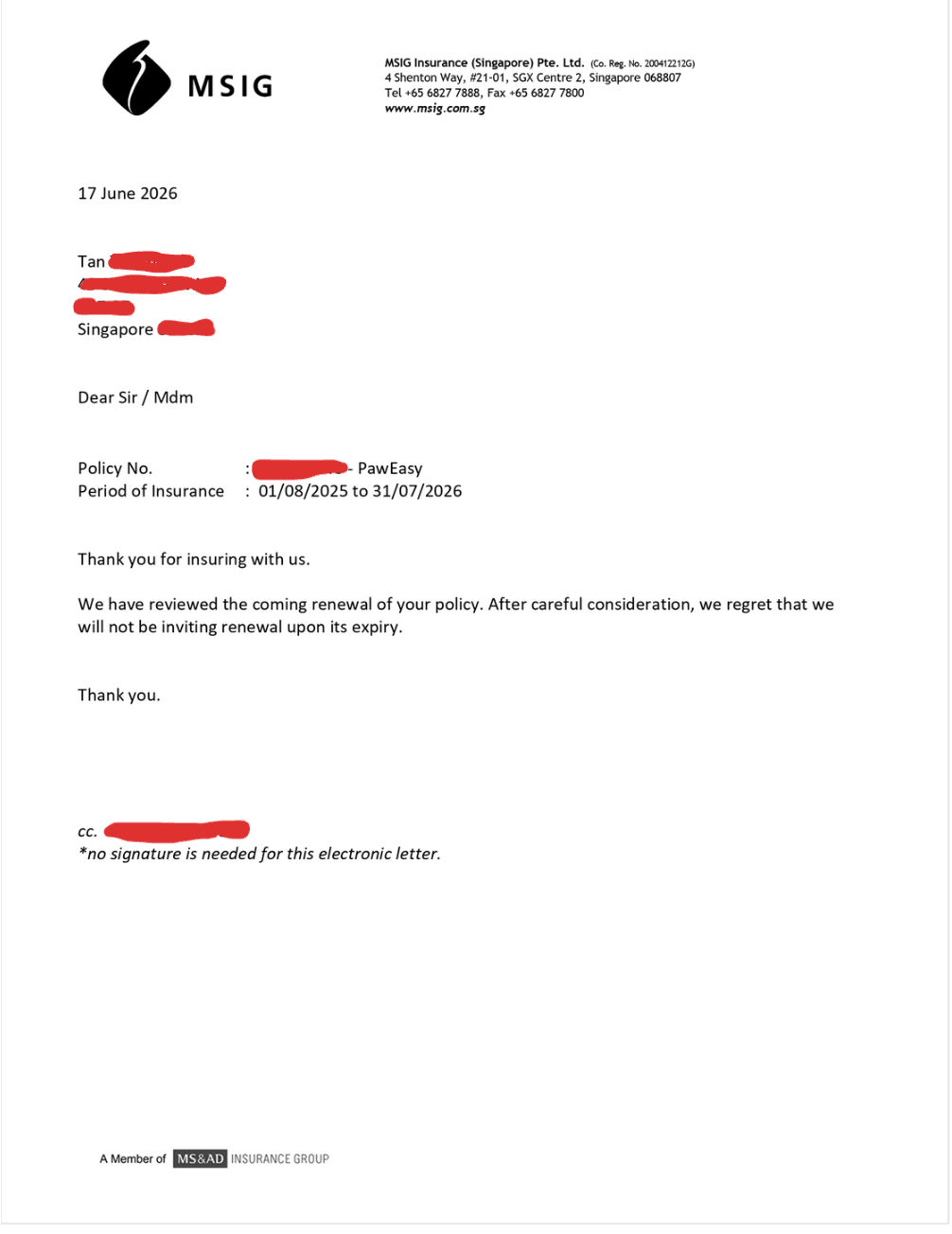

Here's the notice I received on 17 June 2026 through my agent:

Do note I haven't receive any official email from MSIG themselves about this non-renewal notice. (as of 18 June 2026)

Renewal and Non-Renewal

The most frustrating part was not only the non-renewal itself, but how the communication unfolded.

I first received what appeared to be an auto-renewal email, which naturally created the impression that my policy had been renewed. Later, I found out from my insurance agent that the policy was actually not going to be renewed.

That left me with a very poor customer experience for one simple reason: the person or system creating the impression of renewal was not the one delivering the bad news afterwards. From a pet owner's perspective, that kind of mismatch feels careless and confusing.

If renewal is still subject to manual review, underwriting review, or some internal assessment, then automated renewal messaging should arguably not be sent before that process is fully settled. Otherwise, it creates false assurance at the exact point when pet owners are trying to plan for continuity of care.

Why This Felt Unreasonable to Me

What made this especially hard to accept was the scale of the approved claims. This was not a case of extreme usage or obviously excessive claiming. Only 2 claims were approved and paid within the span of one year.

From my perspective as a pet owner, that does not feel excessive at all. It naturally raises an uncomfortable question: does this kind of policy work best only for very low-claim customers, where premiums are collected but actual usage stays minimal?

I cannot say with certainty whether this applies to the entire pet insurance industry in Singapore. Different insurers clearly have different products and underwriting approaches, and local comparison pages show meaningful differences in features, age limits, deductibles, and waiting periods across providers.

For context, I also know someone insured with Liberty who reportedly managed to renew despite making 4-5 claims. That does not prove anything conclusive because risk profiles can differ, but it does show how hard it is for pet owners to know what level of claims activity may actually affect renewal outcomes.

The Waiting-Period Problem

This is the part new pet owners should understand before choosing any insurer.

Pet insurance is not easy to switch halfway through your pet's life. Public Singapore comparisons show that waiting periods are common, and they can differ for injury and illness depending on the insurer.

For example, one local comparison lists MSIG PawEasy with a 14-day waiting period for injury and a 60-day waiting period for illness, while other insurers in the same comparison are shown with one-month injury waiting periods and three-month illness waiting periods. More broadly, many pet insurance plans also exclude pre-existing conditions, which makes switching more painful once any medical history starts to build up.

This is where the real risk comes in. If insurer A drops you in July 2026 and you start a new policy with insurer B in August 2026, anything arising during that new waiting period may not be claimable. If your pet develops a condition during that window, you may end up paying out of pocket first — and that same condition may later become difficult or impossible to insure as a new issue.

Referring to the MSIG PawEasy Pet Insurance Policy under General Exclusions point number 5:

For your pet below six years old at the commencement date of your policy, the following hereditary and congenital conditions that occurs or recurs within the first 12 months of the commencement date or effective date of optional covers added, provided they are not pre-existing conditions:

- Hip and elbow dysplasia

- Luxating patella

- Glaucoma

- Cherry eye

- Intervertebral disk disease (IVDD)

Please note that other hereditary and congenital conditions not listed above are not covered. For your pet six years old and above at the commencement date of your policy, all hereditary and congenital conditions are not covered.

That is why I say the first insurer you choose matters a lot more than many new pet owners expect. Pet insurance is not something you can assume will be easy to replace once renewal uncertainty enters the picture.

Limited Options in Singapore

Another reality is that Singapore does not have a huge number of mainstream pet insurance providers. Local comparison sites repeatedly surface a relatively small group of names such as MSIG, Liberty, Income, Etiqa, CIMB, and a few others depending on how the market is grouped or updated.

So in practice, pet owners are somewhat at the mercy of insurers' underwriting and renewal decisions. When the pool of alternatives is already limited, losing continuity with one insurer is not just inconvenient. It can materially affect what kind of protection your pet can still get afterwards.

My Take

I'm not saying MSIG Pet Insurance is entirely good or entirely bad.

On the positive side, 2 claims were approved and paid, so it wouldn't be fair to say the policy provided no value. However, the process still left a poor impression overall: multiple claims were submitted, but only 2 were approved for the entire year, I received what appeared to be an auto-renewal notice before discovering (from my agent) that the policy would not actually be renewed, and there was a clear disconnect in communication along the way.

As a first-time pet owner, this experience made me question how dependable annual renewal really is, and highlighted the importance of understanding not just what is covered by your plan, but how confidently coverage can continue in the future.

One additional lesson: having a good and efficient agent—especially one experienced with pet insurance claims—can really make a difference. Through conversations with another pet owner who collaborated with Pawwhere, I was fortunate to receive a recommendation for such an agent. I'm grateful for that support, and I believe having an informed and responsive agent can help guide you, clarify renewal expectations, and potentially smooth out confusing claim situations.

Questions Worth Asking Before Buying Pet Insurance in Singapore

Before committing to any pet insurer, these are the questions I think every pet owner should ask:

- Is renewal truly automatic, or is it still subject to underwriting review in practice?

- What happens after multiple legitimate claims in one policy year?

- How are customers informed if a policy is not being renewed?

- Are waiting periods reset when switching insurers?

- Which conditions may not be covered immediately under a new policy?

- How much flexibility do you really have if your current insurer decides not to continue coverage in a small market like Singapore?

Those answers may matter more than the brochure. For many pet owners, the real value of insurance is not just whether the first claim gets paid, but whether coverage remains dependable when the pet gets older and medical needs become more frequent.

FAQs About MSIG Pet Insurance in Singapore

-

Is MSIG PawEasy auto-renewable? MSIG's product page describes PawEasy as auto-renewable. In this reviewer's experience, however, renewal was not guaranteed after one policy year — non-renewal was communicated through an agent after an auto-renewal email had already been received. Confirm renewal terms directly with MSIG before assuming continuity.

-

Does MSIG pay pet insurance claims? Yes, in this case. Two claims were approved and reimbursed within one policy year, supported by claim forms and vet receipts. Not every submitted claim was approved, but valid claims were paid.

-

What happens if MSIG does not renew my policy? You would need to find coverage with another insurer — which typically means new waiting periods, possible exclusions for pre-existing conditions, and a coverage gap while the new policy takes effect. In Singapore's relatively small pet insurance market, that can significantly limit your options.

-

What is the waiting period for MSIG PawEasy? Based on local comparison data, MSIG PawEasy is commonly listed with a 14-day injury waiting period and a 60-day illness waiting period. Always check the latest policy wording for current terms.

-

How does MSIG compare to other pet insurers in Singapore? MSIG is one of several mainstream providers alongside Liberty, Income, Etiqa, and CIMB. Plans differ in coverage limits, deductibles, waiting periods, and renewal policies. See our full pet insurance Singapore comparison guide for an overview.

Note: Pet insurance terms, renewal policies, and claim outcomes can change. This review reflects one policyholder's experience and should not be taken as financial or insurance advice. Always verify current policy wordings and renewal conditions directly with the insurer or an authorised agent before making decisions.